If you’re marketing your fund to European investors, you’ll need to determine the scope of the depositary service you require to be compliant. Eva Devine and Walter Varvara explain how the services differ

For U.S. fund managers planning to raise funds in Europe from European investors, they will, under certain circumstances, need the services of a depositary to be fully compliant with the Alternative Investment Fund Managers Directive (AIFMD).

In general, for U.S. managers, what has come to be termed ‘depo lite’ offers a more flexible version of traditional full scope depositary services. Which service a fund manager needs is determined by which part of the AIFMD governs the AIFM (Alternative Investment Fund Manager) or fund. The AIFMD is the primary piece of legislation governing private markets in the EU.

A good fund administrator will work alongside the depositary service, including flexible integration with client systems and bespoke compliance reporting. There are other considerations too, such as implementation challenges with operational setup potentially complex especially when it is necessary to coordinate with multiple administrators or service providers. There are also regulatory nuances to consider, for example some EU regulators, such as in Germany and Denmark, have ‘gold-plated’ the requirements to appoint a depositary, making them stricter than the baseline AIFMD.

You can read more of our insights into AIFMD here.

A full scope depositary is required under Article 21 of AIFMD for in-scope Alternative Investment Funds (AIFs). This is typically mandatory for EU-domiciled AIFs or those marketed under the AIFMD passport. Find out more about the AIFM passport here.

Depo lite applies under Article 36 or 42 of the AIFMD.

Article 36 permits EU member states to allow EU AIFMs to market non-EU AIFs into the EU without a passport.

Article 42 of the AIFMD permits EU member states to allow non-EU AIFMs e.g. U.S. fund managers, to market EU and non-EU AIFs into the EU without a passport.

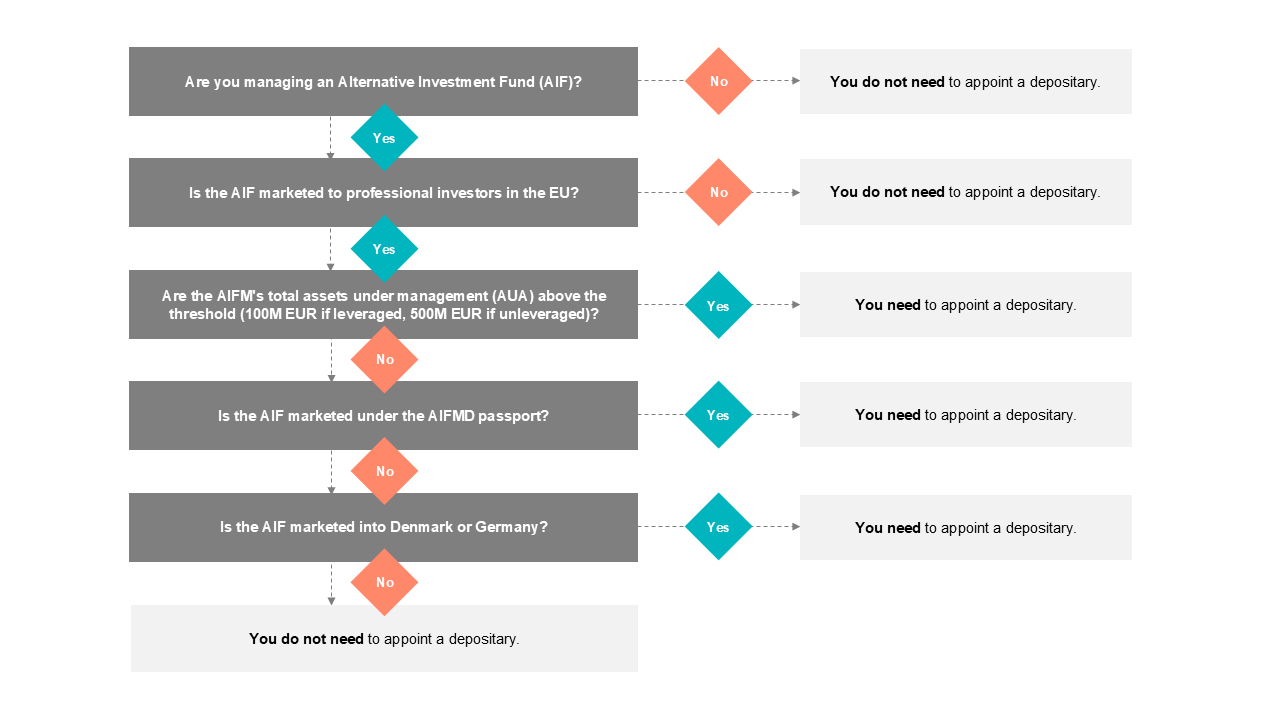

This simple decision tree illustrates how U.S. fund managers can determine their need for a depositary. This is the most likely scenario, but there are exceptions which can be facilitated on a case-by-case basis.

For U.S. managers, determining a fund’s depositary requirements is but one part of a broader checklist, which includes understanding the best route to market, ensuring compliance with key regulation, and maintaining operational best practice. There is estimated to be $750 billion in U.S.-promoted private capital in European centers, and U.S. managers navigating Europe’s complex and highly regulated environment need a third-party provider with comprehensive expertise and experience to streamline the journey. This guide equips U.S. managers with the tools to navigate Europe’s complexities confidently and efficiently.

If you’d like more detailed information about your depositary needs or simply to discuss any of the considerations raised in this article, please contact us.

11 February 2026 Marcia Rothschild

To discover for yourself what makes us the bright alternative and how we can support, please contact Eva Devine, our Group Head of Depositary Services.